Although it may seem a bit complex, CAGR is a simple concept to understand. Let’s look at an example. Imagine that you invest €10,000 for 10 years and, at the end of 10 years, you accumulate €15,000. In this case you will have obtained a total accumulated return of 50%, but what is the real annual return we have obtained?

This annual return is the CAGR, or Compound Annual Growth Rate. We can define CAGR as the real annual interest rate of any financial product.

To convert an accrued rate of return to CAGR, we will use a simple formula composed of the Nominal Interest Rate (NIR) and the frequency of interest payments/collections:

CAGR= (1 + NIR / frequency) frequency – 1

For a more complete definition, the CAGR or Compound Annual Growth Rate is a number that describes the rate at which an investment would have grown if it had grown at the same rate each year and the earnings were reinvested on a compounded basis.

Returning to the previous example. If we want to know the CAGR of an accumulated profitability of 50% in 10 years, we only need to apply the following formula:

[(1 + Cumulative rate) ^ (1 / (End date – Start date))] -1 × 100

E.g.: [(1 + 0.5)^(1/10)] -1 = [1.50^(0.1)] -1 × 100 = 4.13% CARG

To be absolutely precise, the CAGR is the best indicator when you have to measure the growth of your annualized investment when the period is more than one year.

Using the previous example, the Compound Annual Growth Rate (CAGR) of 4.13% leads us to achieve in 10 years a 50% cumulative return. We can see how, by compounding this rate for 10 years, we again obtain the cumulative rate from which we started. The calculations for our example would be:

(1+TAE) ^years -1 = Cumulative Rate

Ej: (1+4,13%) ^10 -1 = 50%

What is the difference between the Compound Annual Growth Rate (CAGR) and the Nominal Interest Rate?

Often banks offer incentives such as “get a 3% return for bringing your pension plan”. Although this nominal return may seem interesting for an investor looking for a relatively safe return, you should consider what it really means for your investment, especially when you are required to keep the deposit for a predetermined amount of time.

If, for example, you are offered an incentive of 3% return on condition that you deposit your investment for a minimum of 5 years, the actual return may be considerably lower. This is sometimes disguised in the fine print. Therefore, the equivalent CAGR may be considerably lower than expected, or desired.

In this second example, the nominal interest rate (NIR) is actually an accrued rate for 5 years so if we apply the above formula:

EX: (1+3%)^1/5-1 = 0.59%

In other words, the 3% nominal return over 5 years becomes just 0.59% annualized.

What initially appeared to be a good investment with a return of 3%, we see how it turns into an annualized return of 0.59%. This return may be low if you compare it to the return that could be obtained by investing in any of our portfolios at inbestMe although, for this, you will have to assume some risk according to your investment plan.

Where to see the CAGR on your investment plan at inbestMe

Investors who have been with inbestMe for more than one year will be able to see the implicit CAGR of their investment plan in their investor panel.

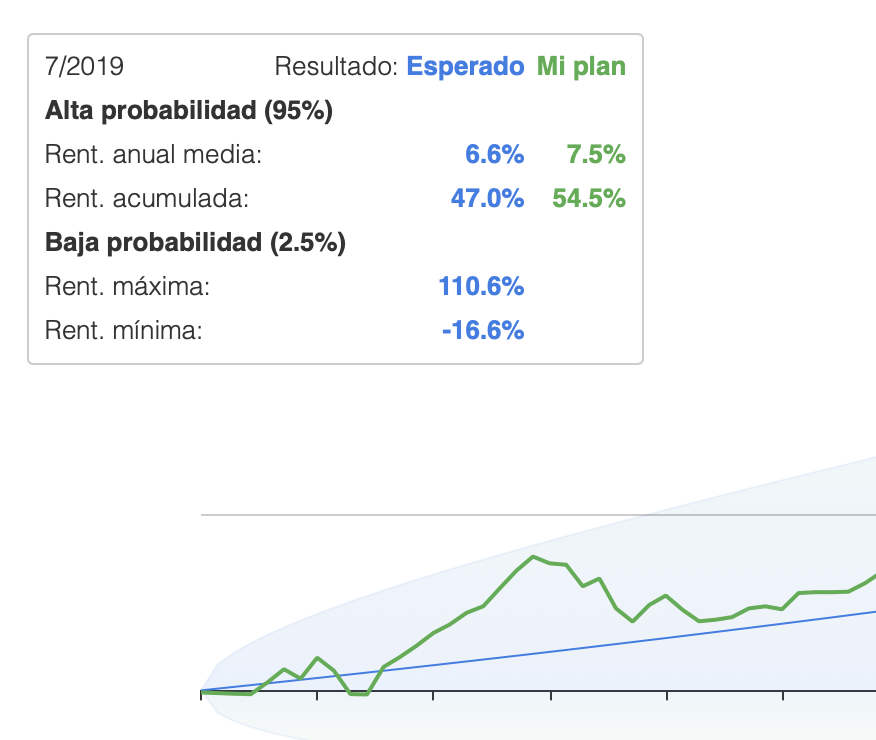

For example, in your plan chart you will see this “Tooltip” or information box:

In the example above, we see in green a cumulative return of 54.5% (vs. in blue an expected return of 47%) and an average annual return or CAGR of 7.5% (vs. 6.6%).

This would be another example of applying the CAGR concept, in this case to a client’s portfolio.

Although this calculation can be done even with a few days or weeks, we have decided to only incorporate it in the client’s information after more than a year, where it begins to be representative.

Once you have been with inbestMe for a year, you will be able to see your CAGR in your client area. Log in to see it.