The meaning of the concept of currency war has been reversed during the last few months.

Until a few months ago the world was basically a deflationary one. Even if now the big issue seems to be inflation, deflation is probably even a bigger problem.

Deflation means that prices tend to fall overtime. In such a situation, individuals tend to defer their purchases waiting for lower prices and companies defer their investments.

But what is even worse with deflation is that the huge amount of debt that economies around the world have amassed increases its real value and becomes not sustainable overtime. This would be likely to push governments to restructure their debt. Basically, they would not be able to repay their financial obligations.

In such a deflationary environment countries liked to have their currency depreciated because that increased the level of internal inflation by increasing the price of imported goods. Keeping rates very low and embarking in quantitative easing policies helped central banks and government to push down the value of their currencies.

Suddenly, after the pandemic, this scenario changed completely and the world become an inflationary one.

The Federal Reserve was the central bank that increased interest rates more aggressively, and this pushed the interest rates difefrential in its favour. This means that US interest rates became significantly higher than the ones of the other developed countries, and capitals tend to flows towards countries where they receive a higher remuneration.

Other central banks followed but the higher rates in the US, coupled with some safe heaven flows towards the dollar that tends to profit from periods of uncertainty, pushed the US dollar higher at the expenses of the other countries.

These countries now see a completely different picture from the one of some months ago. Now a weak currency contributes to import inflation from abroad.

So the meaning of currency war has changed completely. Now everybody want a stronger currency while until recently everybody wanted a weak currency. This is because a strong currency helps to contain inflation and viceversa.

After a few years in which central banks did not intervene in the currency markets they have started to intervene again in the market buying their currency to sustain its value. In particular Bank of Japan and the People Bank of China are intervening to sell dollars and buy their currency.

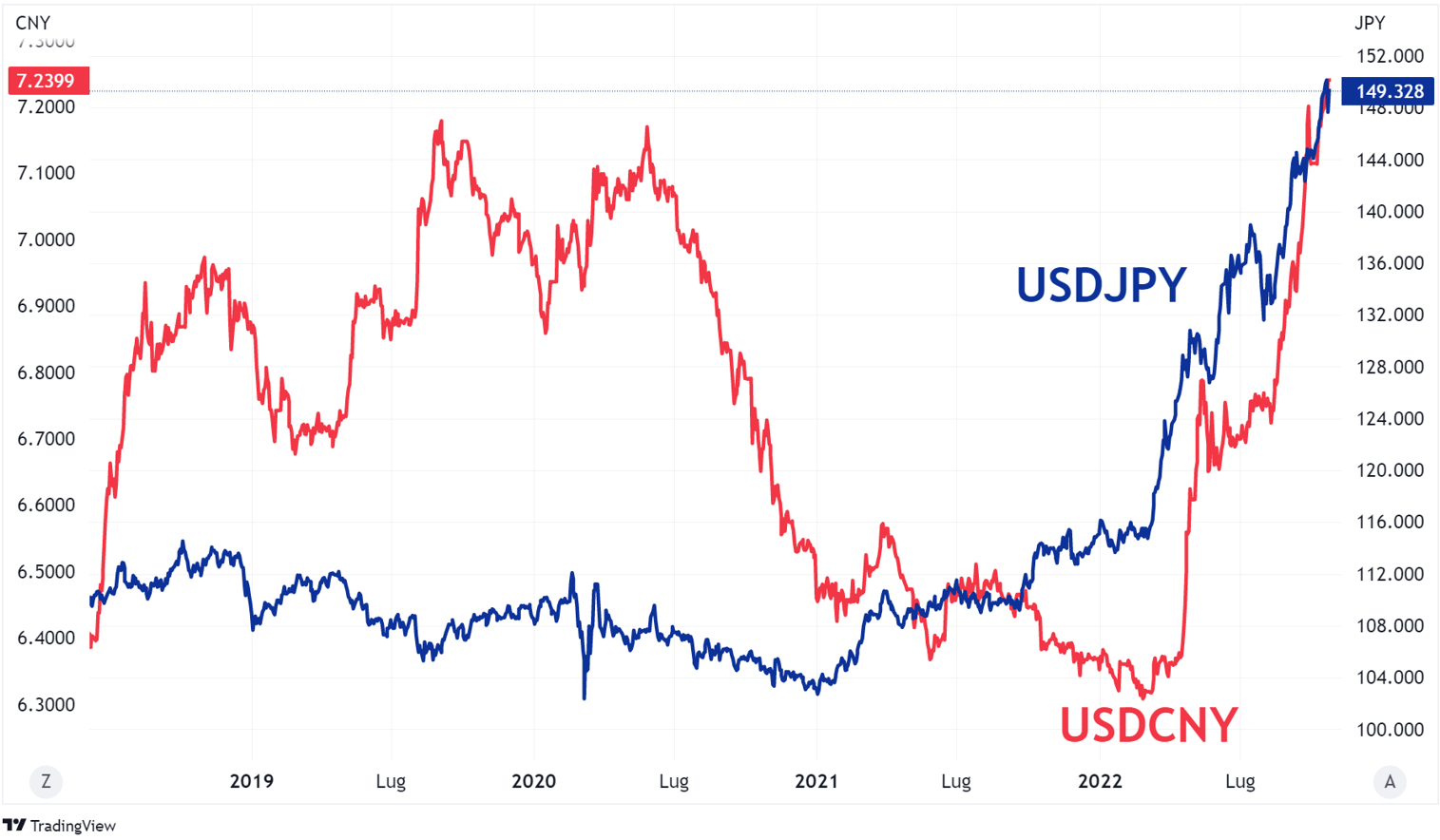

The graph above shows how the yield of government bonds have moved in favour of the US in the last few months. This has pushed higher the value of the dollar against the Japanese and the Chinese currency (graph below).

Bank of Japan intervened in September to support the yen and did it again last week. The central bank intervened by selling dollars and buying yen. This was supposed to lift the value of the yen. Apparently more than 20bn dollars were sold in September and around 30bn last week.

The graph below shows the reaction of the market during last BOJ intervention.

Is currency intervention effective? Well it depends. They show that the central bank is unwilling to see disorderly depreciations of its currency, but it is probably not enough to stop speculation against the currency if not followed by coherent interest rates moves. In other words, if the japanese interest rates remain close to zero, it is not easy to make the yen appreciate.

Moreover, when BOJ intervenes, it is likely to obtain the dollars it needs to sell in the forex maket by the sale of Treasuries that it has in its portfolio. The sale of Treasuries pushes their prices lower and their yields higher, making the difference in interest rates between US and Japan even worse.

Currency interventions are much more effective when different central banks intervene in a coordinated way. For example, if the Federal Reserve intervenes together with BOJ to weaken the dollar, that would be a much stronger signal.

Probably the time is not mature yet for a coordinated intervention, as a strong dollar still helps the US to contain inflation. Probably, the US might be willing to cooperate in weakening the dollar when its strength become a problem in terms of global financial market stability.

A too strong dollar puts under strain the other countries that are obliged to hike quickly interest rates not to see their currency depreciating too much versus the dollar. A too strong dollar also put under strain all those countries and corporates that have to repay liabilities in US dollars. So, a too strong dollar is certaily becoming a source of global instability, and the new currency war will be aimed at defending the value of currencies against the dollar.