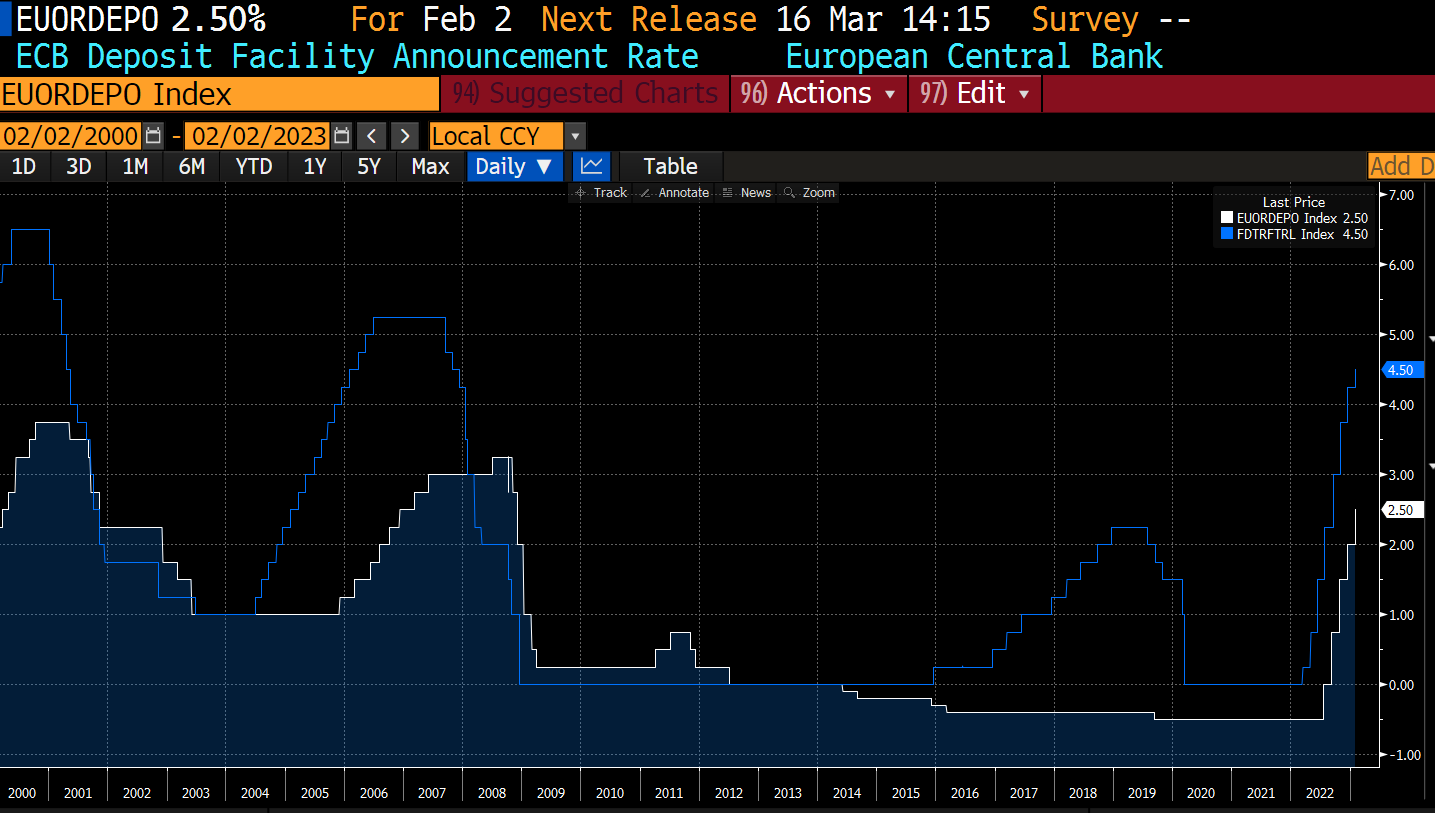

As expected, this week, central banks executed another round of interest rates hikes. This is the last one of a series of very quick hikes that they decided in order to regain the control of inflation. The Federal Reserve raised official rates of a total of 4.50% since last year, and the ECB increased interest rates for a total of 3.00%.

You may be interested to read more about the different official and bank interest rates in Europe or in the USA.

Why do central money hike interest rates to slow down inflation?

Interest rates can be though as the cost of money. By pushing the price of money up, people will have an incentive to save more and spend less. They will be in fact remunerated with a better rate of interest to invest now and defer their expenses to the future. This will decrease the consumption and the upward pressure on prices.

At the same time, for individuals and business will get more expensive to get financing. This will decrease the investments in the real economy that will slow down its growth. This will also tend to contain the upward pressure on prices.

What are the costs of hiking interest rates?

Central banks hike interest rates to slow down the economy and diminish the upward pressure on prices. There are however some costs associated with slowing down the economy. Generally, this means less business activity and more unemployment. This is certainly a remarkable social cost of a restrictive monetary policy.

Central banks have to be very careful in balancing the benefit and the costs of hiking interest rates. During the last months for central banks, the goal of keeping inflation in check has been perceived as more important than the goal of economic growth. Actually, for the ECB, price stability is the only official mandate. The Federal Reserve has the dual objective of price stability and full employment.

What is the situation with inflation?

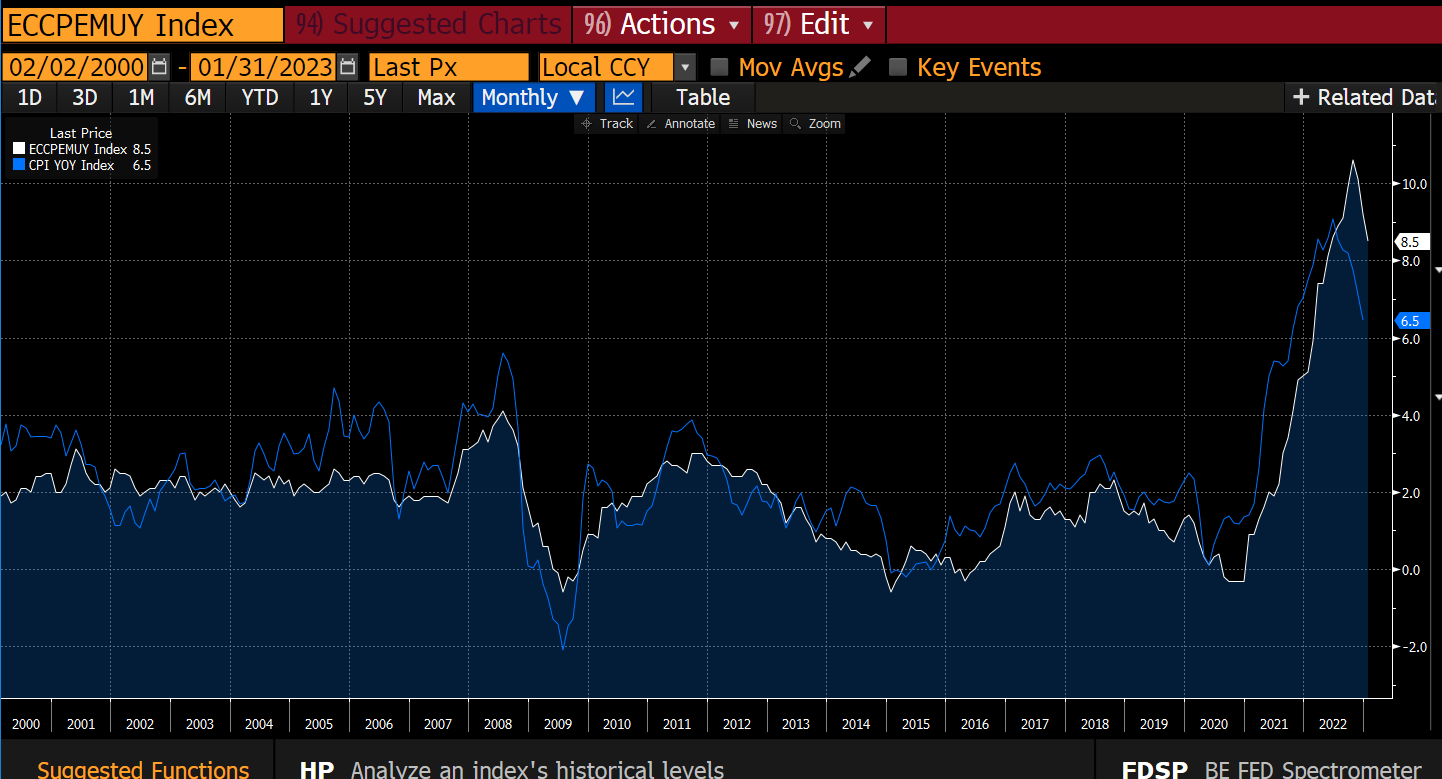

The last interest rates increase take place in a context in which inflation is gradually receding. Prices of energy and commodities, that were the first to increase substantially, are gradually decreasing.

The cost of shipping goods is also decreasing as global supply chains normalize. Inflation remains anyway very far from the 2% objective that almost all central banks have as a long-term objective. Inflation is now at 8.5% in Europe and 6.5% in the US.

What is still of concerns for central banks is that, although inflation is slowing down for those prices that changes very often, such as energy for example, is that it still remains high for prices that change less frequently. In this context, particular attention is devoted to labour costs, as an increase in salaries could make inflation more structural and less temporary.

Should we expect more hikes from central banks?

The effect of a change in interest rates in the real economy is not immediate. It takes some time before its effect becomes visible. So, we can expect that the effects of the last rates increase will operate with some sort of lags on the economy.

After such a rapid increase in rates, and with the economy that is already showing some signs of weakening, it is likely that central banks will soon pause their hikes and observe the lagged effects on the economy, otherwise they risk hiking more than needed and push the economy into a recession.

The economy is not an exact science, so there is no way to know in advance the exact effect of a monetary policy action. So it will have to be carefully evalued against the evidence coming from the economy.

Presumably, the Federal Reserve is quite close to the point at which it will stop and look at the effects of the interest rates on the economy.

On the contrary, the ECB started later to hike rates and has still some room left. Christine Lagarde said that they intend to hike by 0.50% more in March. After that date the decisions will depend on the data coming from inflation and from the economy

Interest rates landscape has totally changed

In any case, we can say that the interest rates global landscape since one year ago has massively changed. We come from a world of negative or near zero interest rates all over the world. Now interest rates, even for short term maturities, are much more interesting.

In an economic environment that remains very uncertain, parking money in short term interest rates instruments is becoming more attractive. For example, in Europe you can easily get returns above 2% to keep money in instruments with very limited risk. In the US, you get return above 4%. This certainly makes a big difference compared to last years when you were obliged to buy very risky instruments to get some results.

inbestMe Savings Portfolio yield rises with official rates

FED rate hikes (US/dollar) are effective as of 2/2/2022, the day of the US central bank’s decision.

ECB (Eurozone) rate hikes will be effective as of 8/2/2022.

The inbestMe Savings Portfolio has been designed to automatically benefit from these rate hikes.

In the coming days, we will be able to confirm definitively how these official rate hikes will be passed on to the Savings Portfolio’s variable yields.

Yes, we can advance that they will be:

- around 1.90% in Euros

- around 4% in dollars.

We will confirm these new (variable) yields between February 10 and 15.