During 2022 we have witnessed a huge volatility in bond markets and also the forex market had some important moves.

The euro against the dollar touched a low of 0.95 this summer and is now back above 1.08.

What pushed the euro lower and what is going on now?

Well, let’s start by saying that the dollar is a safe heave currency that tends to appreciate in conditions of panic. That was what happened after Russia’s invasion of Ukraine.

The global economy is very dollar-centric as the dollar is the most important currency that central banks around the world use to keep their reserves and is the currency that is generally used to invoice international trade.

Many emerging markets governments and corporates issue debt in dollars because is easier to find buyers of dollar bonds than buyers of bonds denominated in local currency.

This high demand for dollars gives to the US a big privilege as it makes easier to finance the huge budget and commercial deficit.

The problem is that when there is a rush to reduce risks and to deleverage the dollar comes in high demand and put the global financial system under stress. Think, for example, to emerging market countries that have to repay a debt in a currency that gets stronger.

This is a bit what happened last summer. Dollar started to appreciate until the global financial system come under stress. Some countries, such as Japan and China, intervened in the forex market selling dollars and buying their currency.

Starting from the autumn, the situation changed. The panic receded somewhat and other countries started to raise their interest rates as well. This helped to sustain the respective currencies.

In the graph below it can be seen that the interest rate differential between the USA and Europe became less unfavourable to the euro during the last few months.

The yield of the 2 year Treasury was around 2.80% higher in the US than in Europe in August and is now “only” around 1.60% higher. Money tends to fly towards those countries that offer a better remuneration and this increases the demand for their currencies.

The fact that the advantage of the dollar in terms of return offered to investors decreased helped the recovery of the euro.

Now the FED is expected to slow down its hikes in rates while the ECB might continue for longer. This could compress further the differential in interest rates.

What happens to the currency then?

After such a strong rally since this summer it is likely that the euro will breath and retrace some of the gains.

But over the medium-long term it is likely that the dollar might continue to have some headwinds. It is in fact well know that many countries that are not aligned with the US want to diversify their currency reserves out of the dollar.

Certainly, at the moment, there is no other currency that can substitute the dollar. Sometimes the yuan is used for international trade among countries that aim to de-dolarize their invoicing but this is quite marginal and the Chinese currency does not seem mature to become a reserve currency or a widely used currency for invoicing international trade.

Anyway, it cannot be completely dismissed the fact that a large part of the world is trying to decrease its holdings and its use of the dollar.

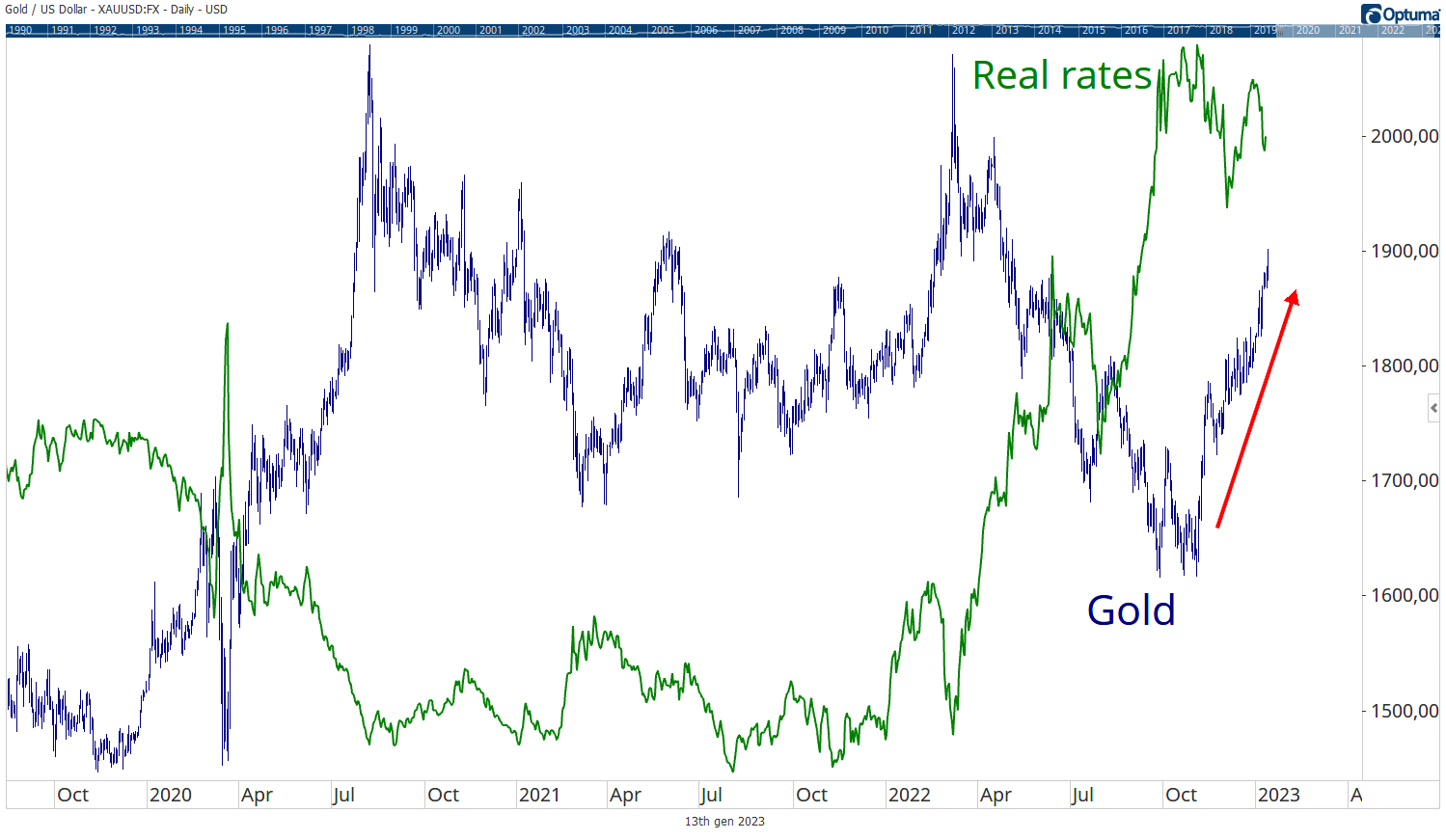

This probably also explain the increase of the price of gold during the last months that has abandoned its usual negative correlation with real interest rates and has continued higher despite the increase in real rates. This is probably due to the large amount of gold bought of those central banks that prefer to detain gold instead of dollars.

It has also to be considered that these countries such as China and Saudi Arabia for example are also the countries with the largest commercial surpluses which means that they have some foreign currency incoming as a result of the fact that they export more than they import that they have to invest and they will probably now diverting this sums out of the dollar. Until some time ago they were instead happy to buy Treasuries.

So, all in all, the world still remains dollar-centric and no other currency is mature to substitute the dollar as reserve currency but the fact that finance started to be used as geopolitical weapon might give rise to some alteration of the previous equilibrium.